Property Taxes, Revenue Sources and How Much Your Municipality Is Worth

- Share

- Tweet

- Pin

- Share

More from the Door County Budget Project>>

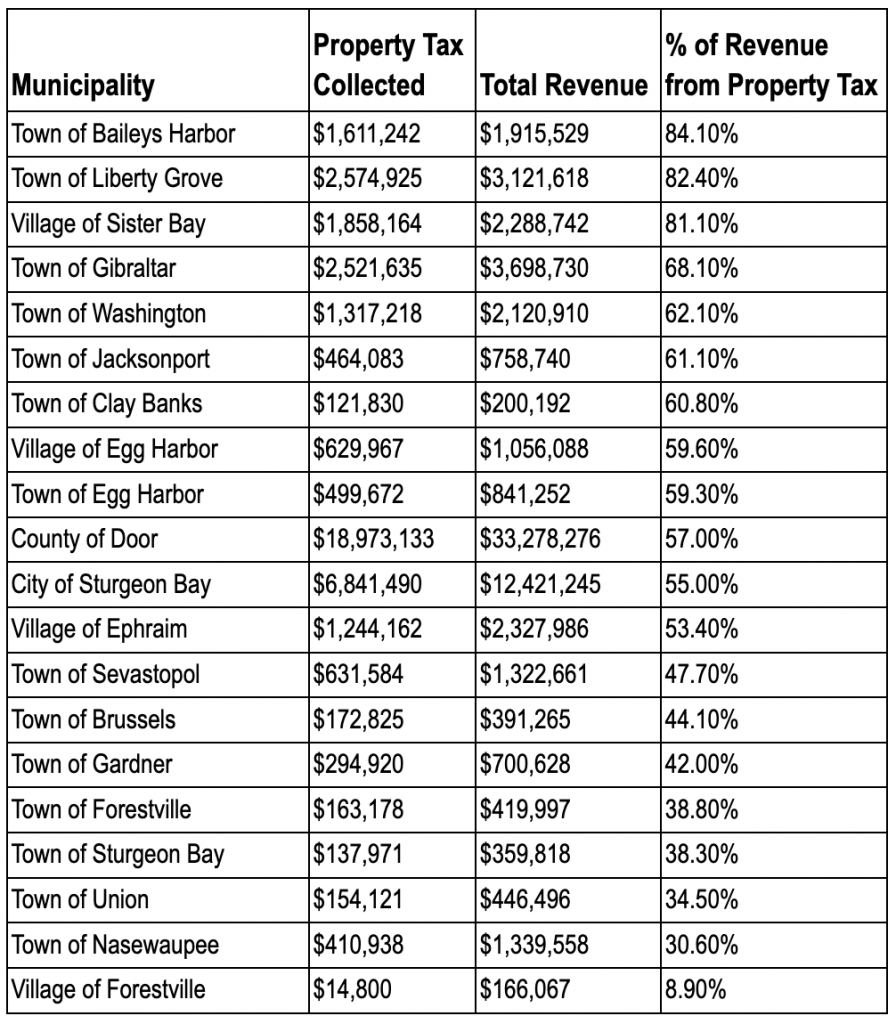

Wisconsin municipalities have various revenue sources to fund services, but they rely heavily on the property tax, deriving some 42.2% of their revenues from it. That is more than any other Midwestern state and nearly twice the national average of 23.3%. In Door County, that proportion is often more than 50%, with some communities generating more than three-fourths of their revenue from the property tax.

This reliance on the property tax is primarily due to two things: declining levels of state aid and restrictions on other possible revenue sources. State aid – revenues that are funded in part by the income tax and sales tax – makes up approximately 20% of municipal budgets today, compared to more than 40% in 1980. Meanwhile, Wisconsin municipalities may not levy an income tax and are restricted on the level of their sales taxes, both of which are significant sources of revenue for municipalities in other Midwestern states.

Context: A municipality funding less of its budget than another with property taxes has other revenue sources. The Village of Forestville, for example, collects the least amount of property tax of all Door County municipalities, yet it also collects from its residents a sanitary tax and a fire department tax that account for 13.1% of all revenues, plus other public charges for services that account for 22.2% of the village’s total revenues.

Conversely, Baileys Harbor and Liberty Grove rely the most on the property tax for revenue. The two towns collect only 0.6% and 1.8% of their revenue, respectively, in public charges for services; neither town has additional tax revenues; and they receive very little from licenses and permits. The same goes for the Village of Sister Bay, which derives only 1.5% of total revenues from public charges for services.

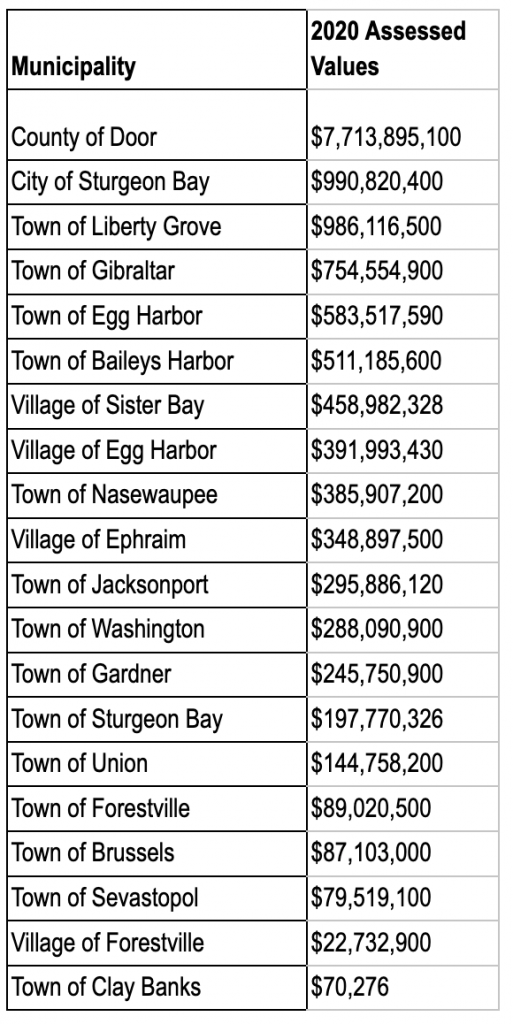

Assessed Valuation

Property value is the dollar value placed on land and buildings for the purposes of administering property taxes. The two commonly used methods of valuing property in Wisconsin are “assessed” and “equalized.”

Assessed valuation is property value as determined by the local municipal assessor on Jan. 1 in any given year.

Equalized valuation results when the Department of Revenue applies an adjustment factor to the assessed value. The adjustment factor incorporates, among other elements, actual property sales in the municipality during the past year and is meant to ensure that each type of property has comparable value, regardless of local assessment practices.

Putting It All Together

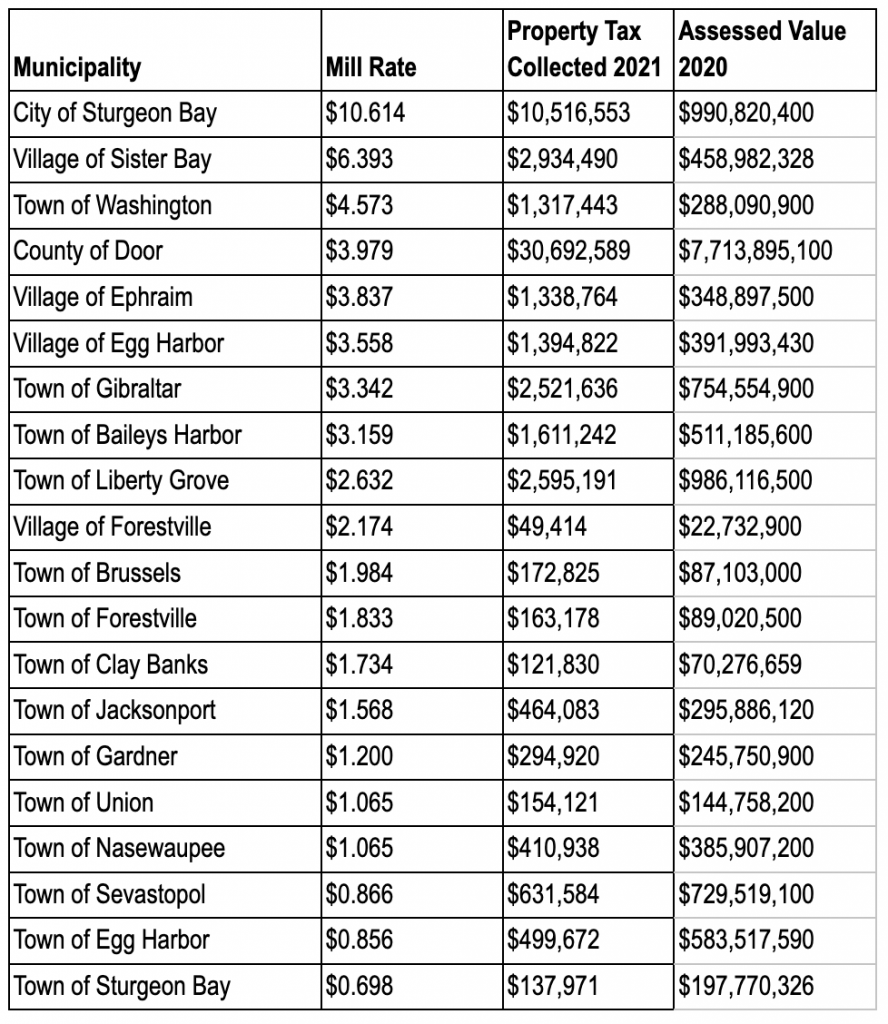

Millage, or mill rate, is a term used to calculate property-tax liability. A mill is one one-thousandth of a dollar, and in property terms, it is equal to $1 of tax for each $1,000 of assessment.

Multiplying your municipality’s mill rate by your property’s value will give you the property tax for that municipality. It will not convey the total tax burden because each taxing authority has its own mill rate (the County of Door, the municipality, the school district and Northeast Wisconsin Technical College).